Refining Margins Face Third-Quarter Struggles

The major refiners will release earnings by mid-November, and the refining margin results will likely disappoint Wall Street.

Most analysts anticipate weak 2024 third-quarter refining margins, and earlier in October, ExxonMobil, BP and Shell warned of lackluster earnings potential.

ExxonMobil said lower oil prices during the third quarter would reduce its earnings by anywhere from $600 million to $1 billion. Lower refining margins were expected to have a similar impact. BP said it expects a $400-600 million hit from soft refining margins.

Shell said that it expected its refinery utilization rates in the third quarter to come in somewhere between 79-83% after forecasting 83-91% in early August. The lower utilization was due to turnarounds in the Netherlands, Germany and U.S. Shell moved up maintenance at its 250,000 b/d Norco refinery in Louisiana after a power outage stemming from Hurricane Francine shutdown a hydrocracker there.

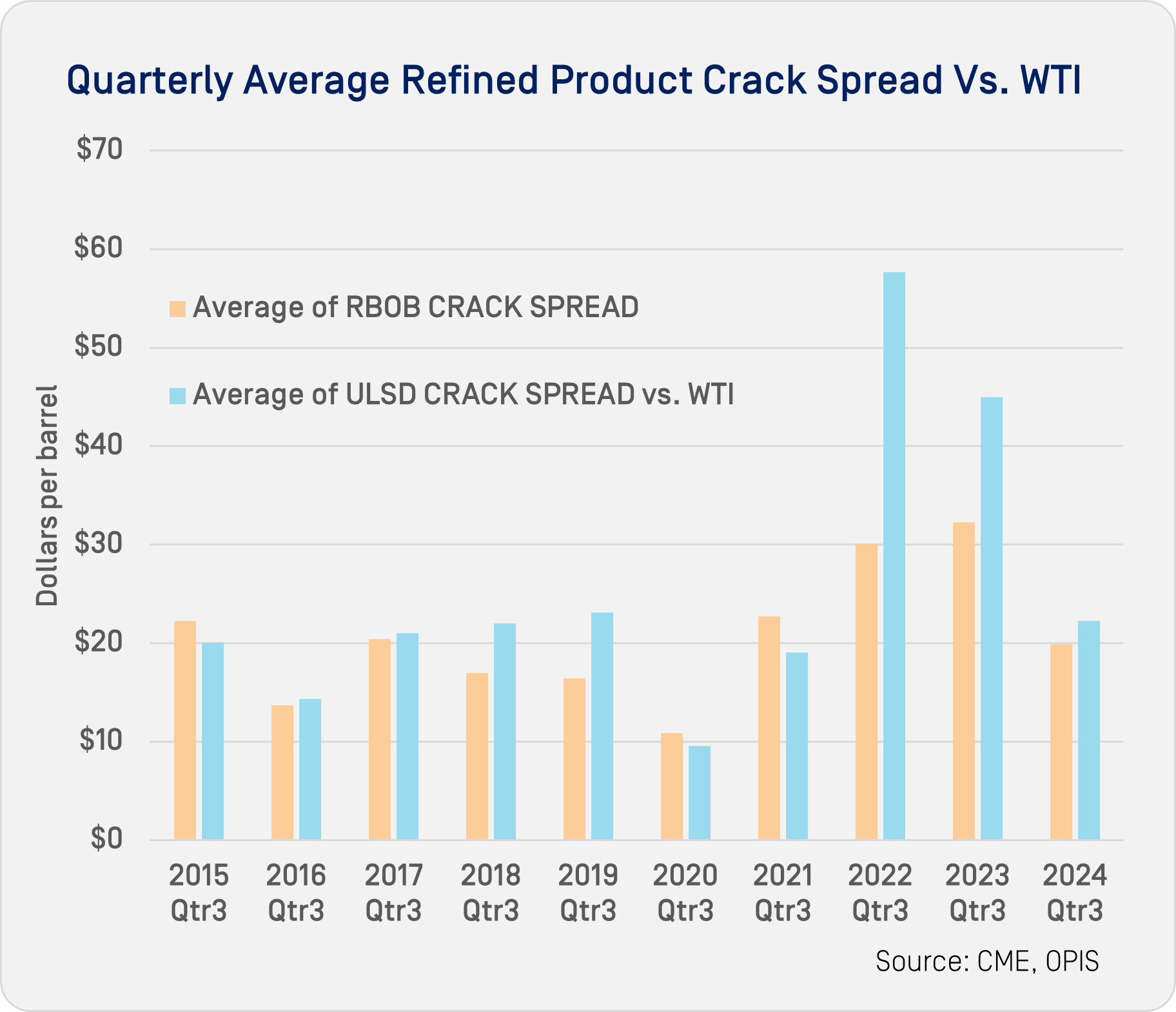

After the outsized refining margins of 2022 and 2023, the search for what a mid-cycle margin might look like may have been found.

Based on NYMEX WTI, RBOB and ULSD futures, the average RBOB crack spread in the third quarter was $19.94/bbl, which is down roughly 38% or $12.35/bbl from the 2023 RBOB crack spread of $32.29/bbl.

Based on NYMEX WTI, RBOB and ULSD futures, the average RBOB crack spread in the third quarter was $19.94/bbl, which is down roughly 38% or $12.35/bbl from the 2023 RBOB crack spread of $32.29/bbl.

The recently completed quarter’s RBOB crack is also less than 2021 and 2022, but it compares quite favorably with the crack spreads in a five-year span from 2015 to 2019 when the average NYMEX RBOB third quarter crack spread was $17.96/bbl.

It would be nearly impossible for diesel to have the same third-quarter performance as it did in the third quarters of 2022 and 2023, when the ULSD-WTI NYMEX crack spread averaged $57.64/bbl and $44.97/bbl, respectively. The most recent third quarter came in at $22.26/bbl, a roughly 50% haircut from a year ago.

Like gasoline, the third-quarter NYMEX diesel crack spread compares more closely with the 2015-2019 period. The average crack spread during that five-year stretch was $20.11/bbl, which sees the 2024 third quarter roughly $2/bbl better than that five-year average.

One certainty, though, is that the third quarter was uneven. The quarter started rather strong in July, but the paper crack spreads decreased in value in the following two months.

While the NYMEX crack spreads are typically a good guide for refinery profitability, looking at the seven U.S. spot markets reveals that very few markets achieved what the paper markets had indicated. Throw in the Renewable Volume Obligation costs and some spot markets significantly underperformed versus the paper market.

Like the paper cracks, some markets turned in the same uneven performance with stronger margins at the front end only to see the crack spread fade into the end of the quarter.

On the Gulf Coast, the conventional blendstock gasoline market went from a July average versus light sweet crude oil delivered to Houston of $16.95/bbl to just $1.92/bbl in September. When considering processing costs and the renewable volume obligation costs, it’s not a stretch to say that there were multiple days when Gulf Coast refiners were making gasoline at a loss.

On the Gulf Coast, the conventional blendstock gasoline market went from a July average versus light sweet crude oil delivered to Houston of $16.95/bbl to just $1.92/bbl in September. When considering processing costs and the renewable volume obligation costs, it’s not a stretch to say that there were multiple days when Gulf Coast refiners were making gasoline at a loss.

Overall, the gasoline crack spread on the Gulf Coast averaged $8.77/gal. Gulf Coast diesel also saw a similar pattern with a $22.70/bbl July average eroding to $9.33/bbl and a quarterly average of $14.38/bbl.

The Gulf Coast gasoline and diesel crack spread was down in the neighborhood of 30% from the second quarter.

The West Coast went against the trend seen in the paper markets and on the Gulf Coast, as the average CARBOB margin rose through the third quarter. The gasoline crack, against Alaska North Slope crude oil, certainly appeared to be more pedestrian, especially compared to the first and second quarters of 2024.

Los Angeles saw an average third-quarter CARBOB margin of $18.40/bbl, according to OPIS spot market data. The July average was inside of $12/bbl, which was the lowest month of 2024 so far. By September, the average margin bumped up to $23.72/bbl. The stronger September was thanks largely to softer crude oil prices, as ANS in September averaged $74.44/bbl. At the same time, the average spot price, according to OPIS data in L.A., was $2.3373/gal.

CARBOB refining margins in San Francisco were about 37% better than Los Angeles’s in the third quarter, averaging $25.21/bbl. Like the L.A. market, the San Francisco CARBOB margin was also aided by the falling price of ANS.

While gasoline crack spreads took a step back, those able to process heavy sour crude were faring much better.

Chicago area refiners that process the heavy Western Canadian Select saw CBOB cracks consistently above $20/bbl, with a third quarter average of $22.31/bbl. ULSD versus WCS averaged $26.63/bbl in the third quarter.

Overall, the Chicago 3:2:1 crack spread against WCS, according to OPIS data, averaged $23.75/bbl, which was largely in line with the second quarter. Compared to WTI futures, the 3:2:1 crack spread in Chicago generally trailed heavy sour crude by about $5/bbl.

Of course, gasoline is always cyclical, and in the past two years, refiners have been able to lean on diesel and jet fuel production, which was not the case during the third quarter.

Diesel was a bit more mixed. Some markets, like Chicago, saw the diesel crack improve by a few dollars per barrel from the second quarter to the third quarter. Gulf Coast saw the diesel crack drop by more than $5/bbl from quarter to quarter.

The San Francisco market saw the largest pullback in the third quarter, dropping $9/bbl. California markets have seen legacy hydrocarbon-based diesel being replaced at a significant clip by renewable diesel. However, even with the incentives, renewable diesel also saw some of its margins clipped in the third quarter.

It should also be noted that the third quarter is among some of the softest periods for diesel demand.

While there was plenty of discussion of strong air travel during the 2024 summer, refiners did not reap the benefits of the stronger demand in the form of strong pricing for jet fuel.

Every spot market saw jet fuel prices drop from the second quarter to the third with the crack spread falling anywhere from about $3/bbl to as much as $8.40/bbl. As a result, a 6:3:2:1 (six barrels of crude oil yields, 3 barrels of gasoline, 2 barrels of diesel and 1 barrel of jet fuel) in several markets were down $3 to $6/bbl in multiple markets.

Besides product weakness to close out the third quarter, the renewable volume obligation cost was seen going up throughout the quarter.

During the third quarter, the RVO averaged 9.27cts/gal or $3.89/bbl, which is the highest quarterly average of 2024. While the third quarter for refining margins are off to a good start, picking up from where September averaged, the RVO is also moving higher as the month to date average for October stands at 10.36cts/gal or $4.35/bbl.