Shaping the New Norm of Elevated U.S. LPG Exports to Europe

OPIS analysis suggests that protracted robust premiums for natural gas over liquefied petroleum gas (LPG), a tightening of supply in East Europe since Russia’s invasion and rising demand from the petrochemical sector are shaping a new norm of elevated U.S. imports into Northwest Europe, as the flood of U.S. LPG exports to Europe over June and July reach multi-year highs.

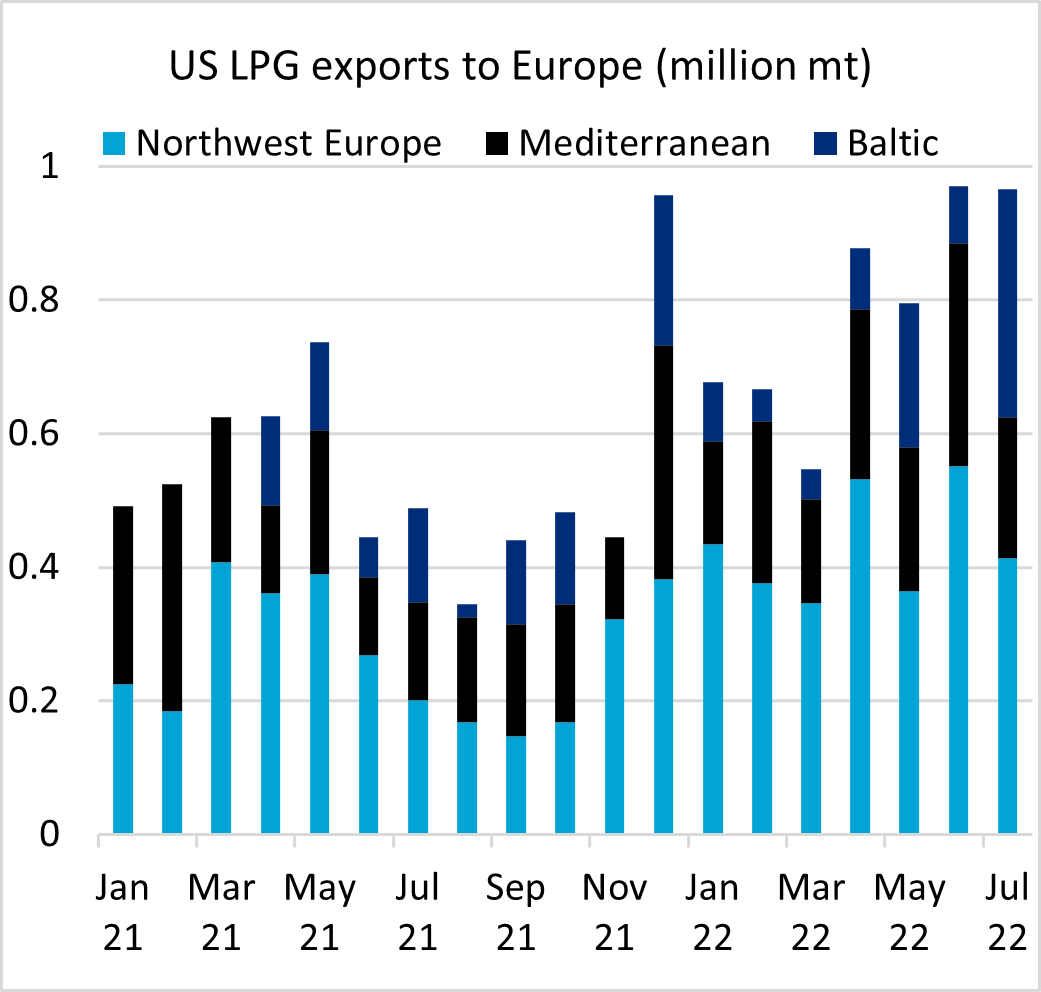

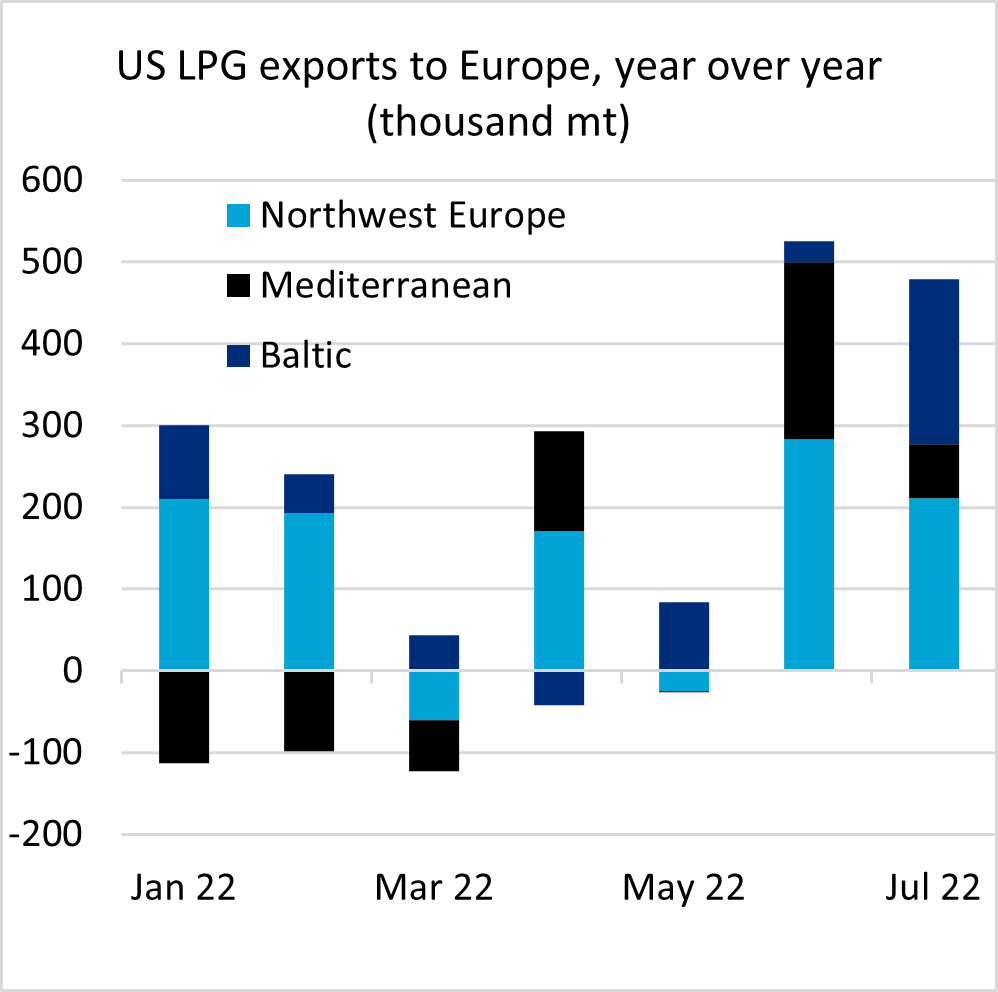

Since the start of Russia’s invasion of Ukraine, European LPG imports from the U.S. have risen by a total of 1.23 million mt on year by mid-July, equivalent to 27 more Very Large Gas Carriers (VLGCs) worth of LPG arriving over the space of five months. U.S. exports to Europe increased by 525,000 metric tons in June and by 479,000 mt in July, year over year, each month a new multi-year high going back to 2014, according to OPIS data. The rising imports come despite heavier on year steam cracker turnarounds in Europe weighing on petrochemical demand needs from March through to late-June.

Source: MINT, OPIS

Source: MINT, OPIS

Gas prices and war will continue to curtail domestic output

Since September 2021, natural gas prices in Europe have commanded a sizeable premium over both propane and butane (LPG) on a heat equivalence basis, an atypical occurrence as purity Natural Gas Liquids (NGLs) such as propane and butane which require higher energy and capital inputs to yield and store, traditionally cost more than natural gas.

Following natural gas’ steep premium to LPG, gas processing plant operators in the North Sea, such as Gassco, began reinjecting LPG and other NGLs into the natural gas stream from the first half October where they found more value, according to Gassco in December 2021 and June 2022.

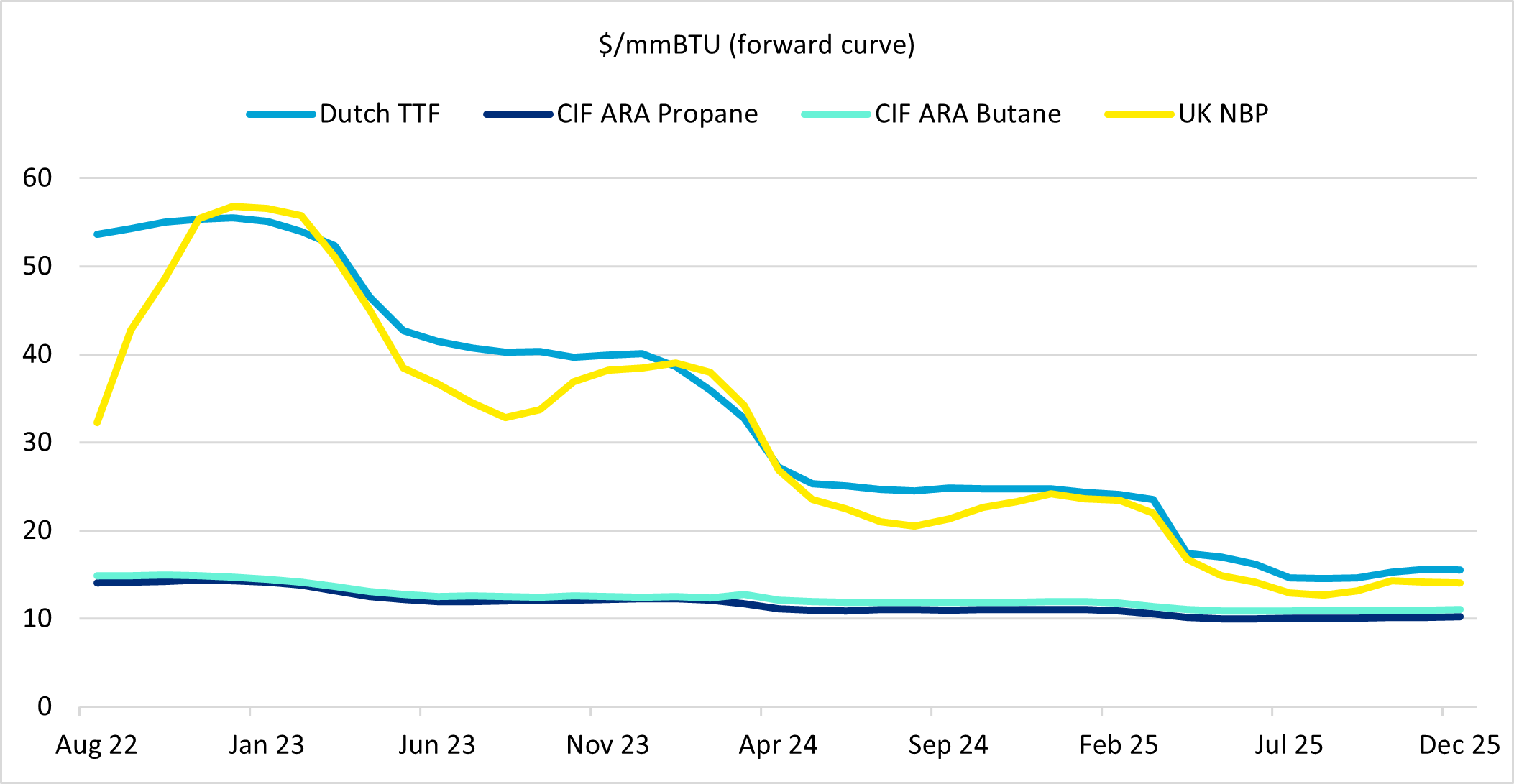

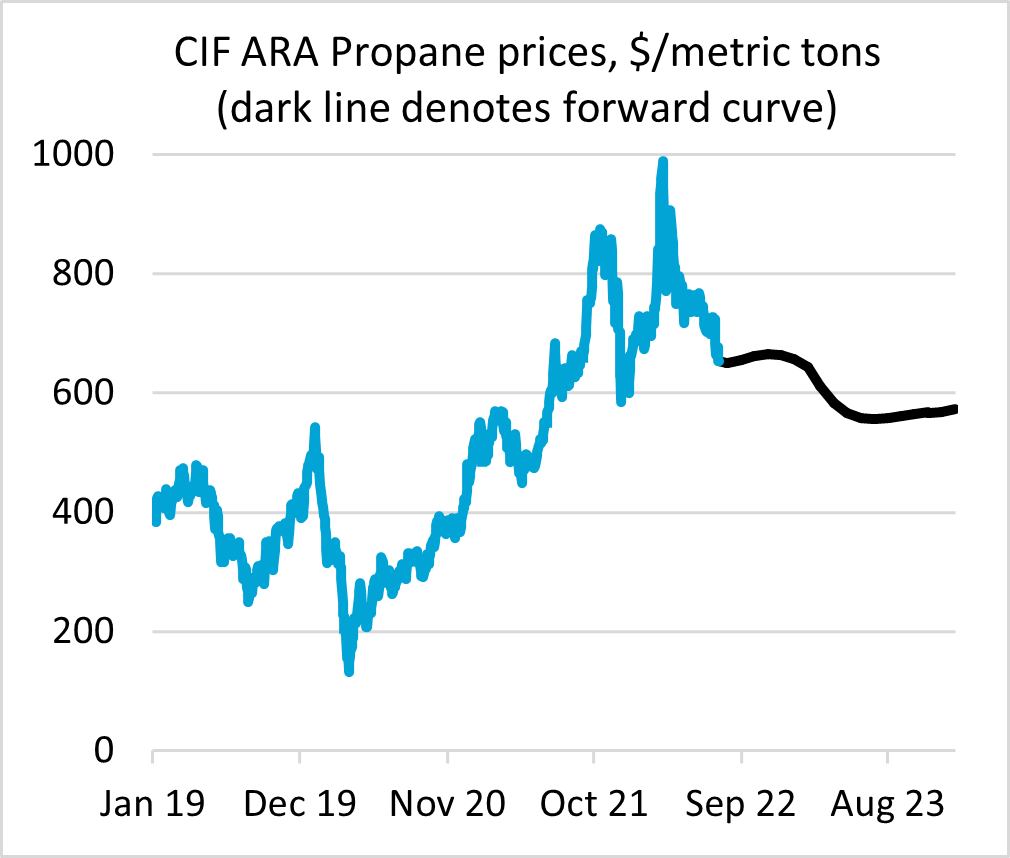

And gas plants in Europe are set to continue reinjecting LPG into the gas stream into the foreseeable future. Data from the Chicago Mercantile Exchange show the forward prices of natural gas at a price premium to both CIF Amsterdam, Rotterdam and Antwerp (ARA) propane and butane prices on a $/mmBTU basis until at least December 2025.

Source: Chicago Mercantile Exchange Group (CME), OPIS

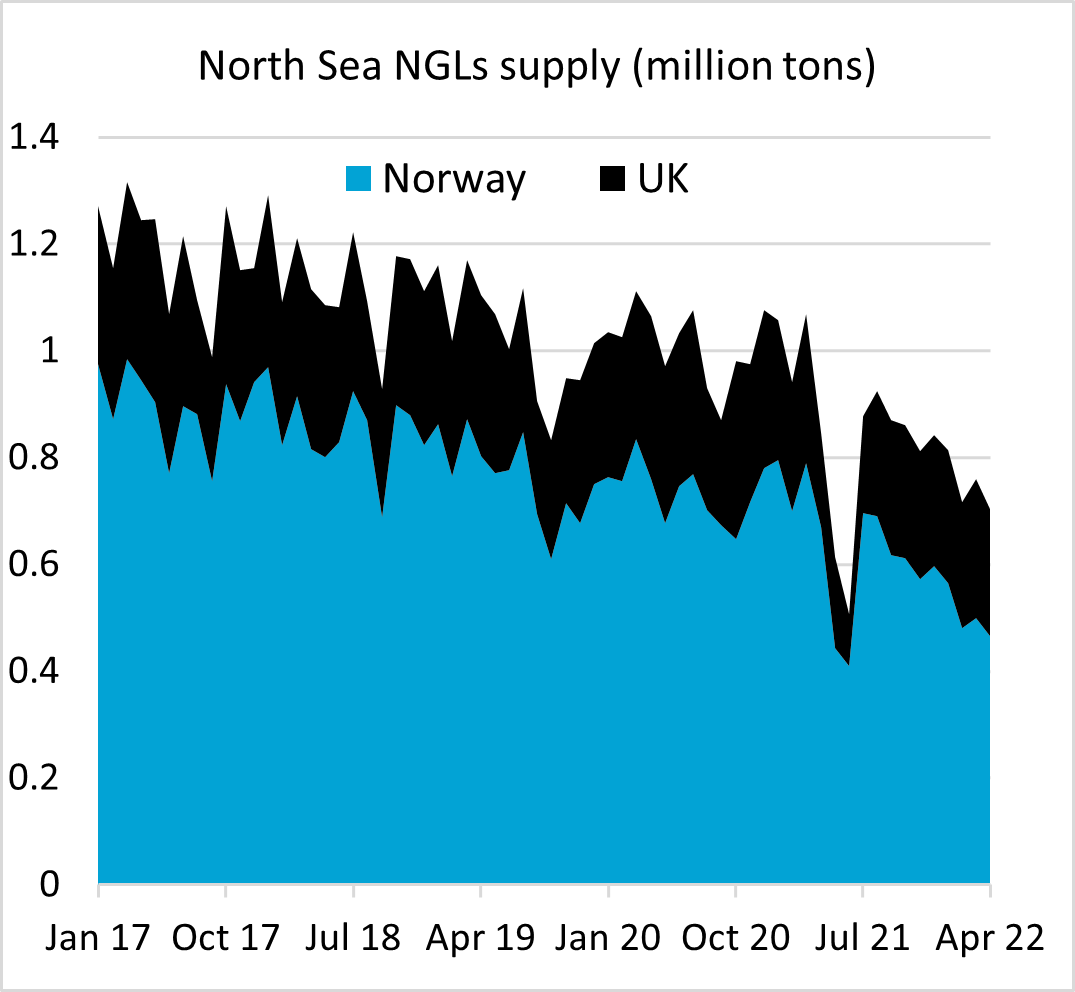

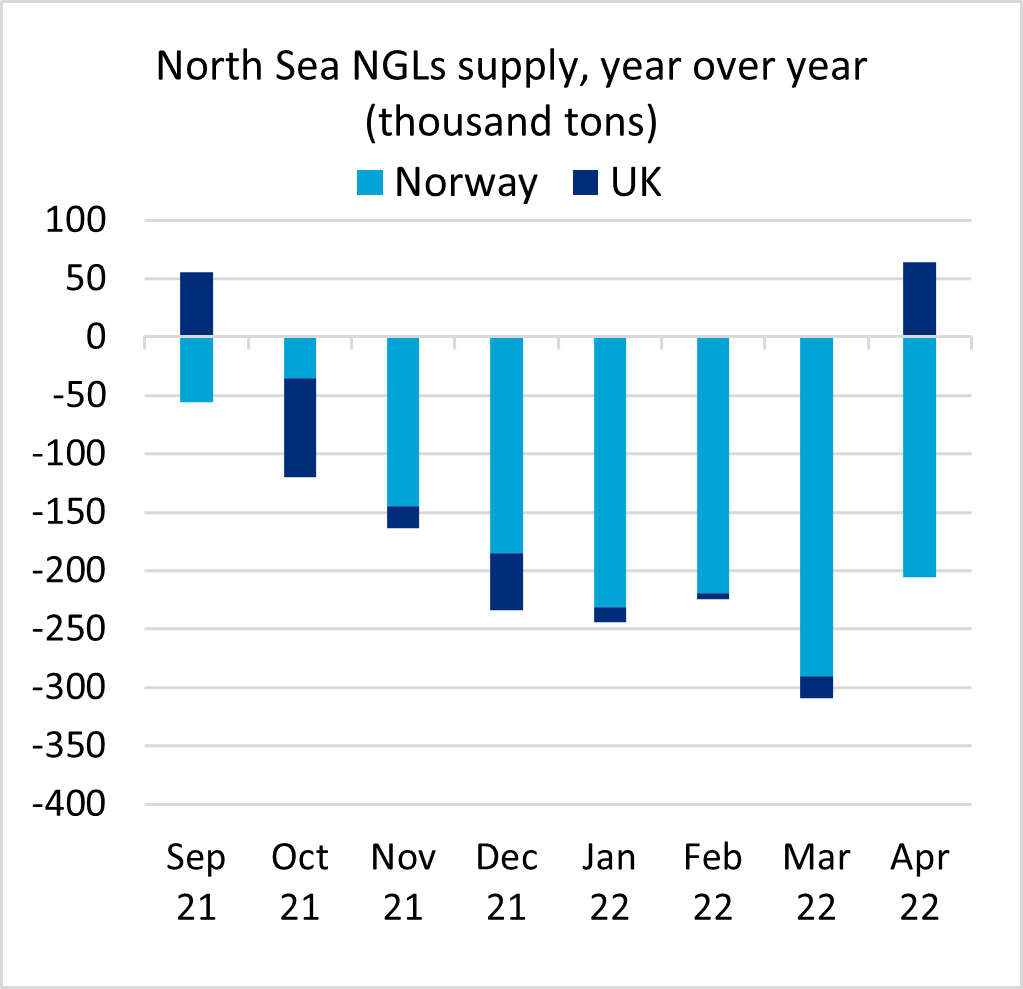

Meanwhile, European LPG production via gas plants has been falling by an average of 88,000 mt/month year over year since October 2021 to April 2022, according to Joint Organization Data Initiative (JODI) data and OPIS analysis.

U.K. and Norwegian official governmental data show that NGLs supply has fallen by an average of just over 205,000 mt/month on year since October 2021 to April 2022, suggesting a decrease of LPG supply from North Sea gas plants of just under 43% since natural gas’ premium to purity NGLs emerged.

Source: Norwegian Petroleum Directorate (NPD), UK Department for Business, Energy & Industrial Strategy, OPIS

Source: Norwegian Petroleum Directorate (NPD), UK Department for Business, Energy & Industrial Strategy, OPIS

In Europe, the majority of LPG supply is derived as a by-product of crude mineral oil refining, accounting for 74% of Europe’s LPG supply on average over the past five years, according to JODI data. As such, refinery operations play an outsized role in inland markets especially when determining regional balances.

The natural gas premium to LPG has incentivized refiners to consume the LPG they yield as a by-product of refining to replace some of the natural gas purchases needed to power furnaces and other secondary endothermic processes.

Moreover, partial or complete refinery rationalizations across the continent since the start of 2020, largely due to COVID-19 related lockdowns, will reach almost 0.8 million b/d by end-2022, capping refinery runs and thus LPG output, despite improving oil product crack spreads/margins following Russia’s invasion of Ukraine.

Adding to tightening supply in Europe since end-February 2022 has been Russia’s invasion of Ukraine. Russian halted LPG exports to Ukraine and stopped exports to Romania, Hungary, and Moldova via railcar, forcing importers in those countries to look for new routes to fulfil demand requirements.

Western energy majors have also decided to adopt self-sanctions relating to Russian energy products, leaving ex-Ust Luga parcels struggling to find buyers in the Baltic or Northwest Europe, their typical export destinations.

This has led to buyers in Eastern Europe, especially those based in Poland that has given refuge to Ukrainians fleeing the war, looking to pull in more barrels from western Europe via railcars from the ARA hub – itself reliant on greater volumes of U.S. imports to balance.

Polish buyers have also been importing more barrels from Sweden’s Karlshamn which has the capacity to take Very Large Gas Carriers (VLGCs) carrying on average 46,000 tons of material. VLGCs feeding barrels into Karlshamn are typically U.S.-origin cargo ex-Marcus Hook or the U.S. Gulf coast. The bulk LPG tons are then broken into smaller parcels and shipped on handy-sized vessels into Poland’s northern port of Gdansk, and then railed or trucked to bottling plants and end-users, according to SHV Energy.

The recent squeeze on Russian LPG imports into Europe has exacerbated the trend in recent years of falling Russian exports. Indeed, Russia’s net LPG exports peaked in 2018 at 4.8 million tons and fell dramatically from Q4 2019 onward, following the ramping up of Sibur’s ZapSibNeftekhim LPG steam cracker. This, along with rising domestic autogas demand, shrank Russia’s net LPG length, leaving fewer barrels for exporting to Europe.

DEMAND: In chemicals we trust

At the start, Europe’s tightening LPG balances were partially hidden following Russia’s invasion of Ukraine. A combination of planned Spring turnarounds and unplanned maintenance at flexible-feed steam crackers from March through to mid-June suppressed the potential pull on U.S. barrels needed to fulfil demand requirements if LPG cracking was favored over competing liquid feedstock naphtha.

However, since early-March 2022, propane has largely retained its favorability over naphtha in the feedstock pool due to its significant price discount. Flexible-feed steam crackers typically maximize propane intake when propane is 90% the cost of naphtha or lower, due to differing by-product yields between the two feeds.

Over April-May, cracker maintenance in western Europe peaked, with an average of 18% of ethylene capacity offline during those two months. In June, outages fell to 13.6% of total capacity and July is forecast to fall to further, to a mere 10% of capacity offline, largely due to the ongoing planned works at SABIC’s Wilton ethane cracker in Northeast England, according to data from Chemical Market Analytics by OPIS, a Dow Jones company.

Therefore, as crackers returned from planned and unplanned works sporadically from mid-May onward, Europe’s LPG short became clearer as traders began pulling in substantial volumes of mostly propane on VLGCs ex-U.S. to feed the largely coastal based flexible units.

So, with cracking margins wide in Europe for propane-oriented ethylene plants in June, a slew of VLGCs were booked for not only June but July. However, the strength of demand for U.S. LPG exports arriving in Europe during July may have been overestimated.

Source: OPIS

Source: JODI, OPIS

That’s because in Europe, there’s no publicly traded olefins futures, unlike in the U.S. or Northeast Asia. As such, petrochemical majors with steam cracking assets are not easily able to hedge their margins.

So, while steam cracking margins looked healthy on paper based on term prices, spot ethylene tons were offered at 33% discounts to the CIF Northwest Europe monthly term price in July of 1495 euros/mt in the middle of the month, after July’s term prices had already fallen by 100 euros/mt on month, according to research by Chemical Market Analytics (CMA), OPIS a Dow Jones company.

Propylene spot values have seen similar levels of downward price pressure in July, according to CMA research. Spot propylene was offered at a 27% discount to July’s polymer grade CIF Northwest Europe term price of 1480 euros/mt, itself down by 120 euros/mt on month.

Plummeting notional spot prices suggest margins could struggle even at more competitive flexible-feed crackers in August 2022 if the sizeable olefin discount weighs on that month’s term settlements. If margins are into the red, cracker operators typically lower utilization rates to manage free-cash flow, which then dampens LPG demand.

Less competitive inland crackers, which take naphtha from attached or nearby refineries, should struggle more than their coastal counterparts, with traders already suggesting inland naphtha units were running at below 80% of capacity in July. Naphtha cracking requires more energy than gas cracking and energy costs across Europe remain close to historic highs following Russia’s invasion of Ukraine.

Additionally, the current CIF ARA propane/CIF Northwest Europe naphtha forward curve suggests that naphtha will regain its economic advantage over propane from November 2022 through to end-February 2023, during the seasonal heating period when LPG demand in northern Europe peaks.

Also, the German industrial association for chemicals, the Verband der Chemischen Industrie (VCI), forecasted in July that German production at pure chemicals businesses will fall by 4% year over year in 2022, largely due to the exorbitant energy costs eroding the country’s competitiveness. Germany remains the largest producer of petrochemicals and plastics in Europe.

Thus, in the short term, European LPG demand faces potential risk from softening cracking margins next month weighing on rates combined with falling downstream plastics demand, followed by naphtha pricing itself into the cracking pool from November 2022. If these demand risks come to materialize, European LPG imports from the U.S. will ease from their current record highs.

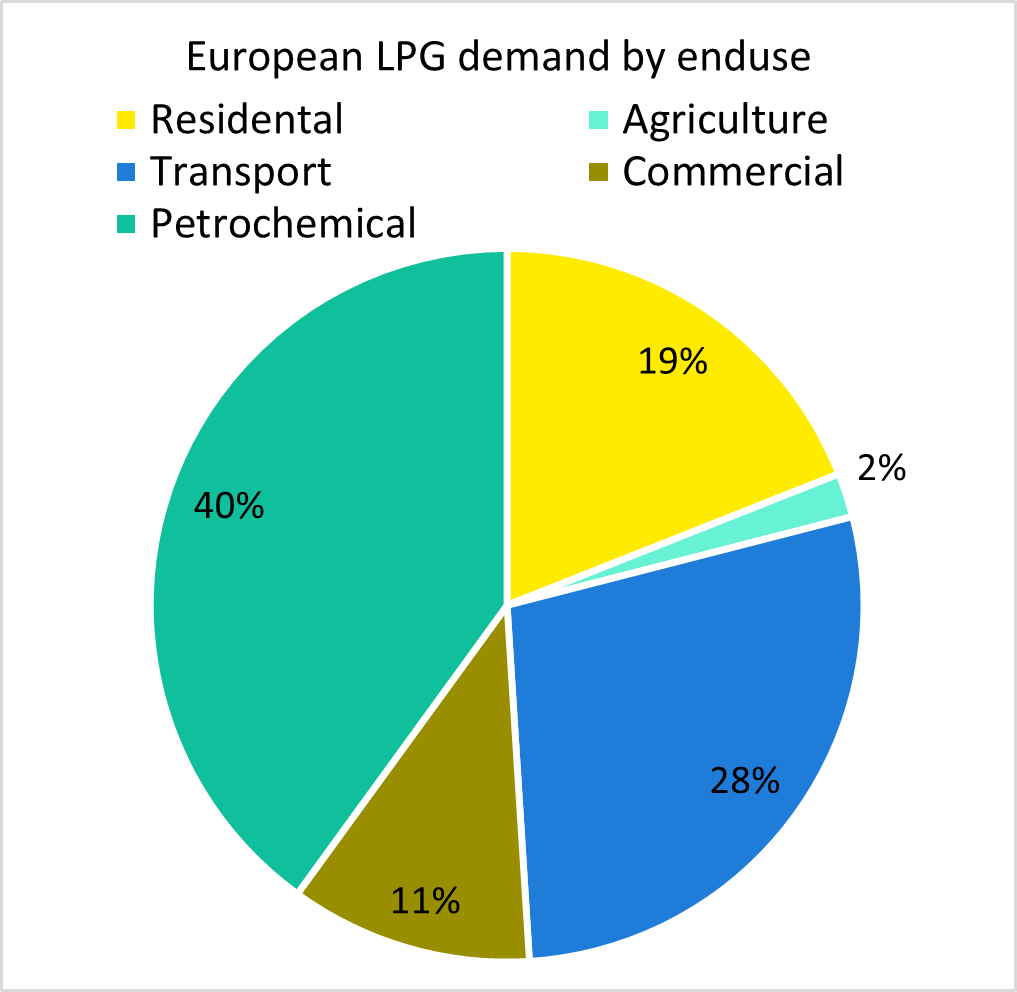

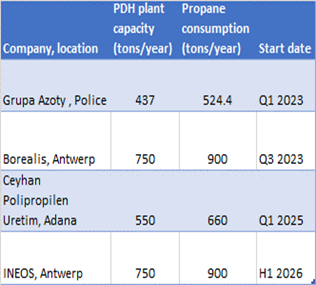

Petrochemical production already makes up the largest segment of end-use LPG demand in Europe. As new propane dehydrogenation (PDH) plants enter service, and as autogas and residential segments lose ground to the ongoing electrification of Europe’s energy system in the medium term, petrochemical production will become increasingly dominant in the European LPG industry (see table).

Source: World LPG Association

Source: Public reports, press releases, OPIS

PRICES: Risky business

Europe’s ever-growing reliance on U.S. imports to balance poses volatility risk to CIF ARA prices as supply-lines are extended. Any shipping or production issues in the U.S. market begin to become more heavily reflected in Northwest European prices with fewer North Sea and Russia volumes on offer to help plug any gap.

With most LPG shipped from the U.S. Gulf coast, the risk of hurricanes disrupting both production and shipping or heavy fog disrupting loadings, means that European buyers could be left waiting longer periods during particularly aggravated weather seasons. Import delays of ex-U.S. material caused by heavy fog in the Gulf coast could potentially be a greater cause of seasonal price volatility than hurricanes hitting production.

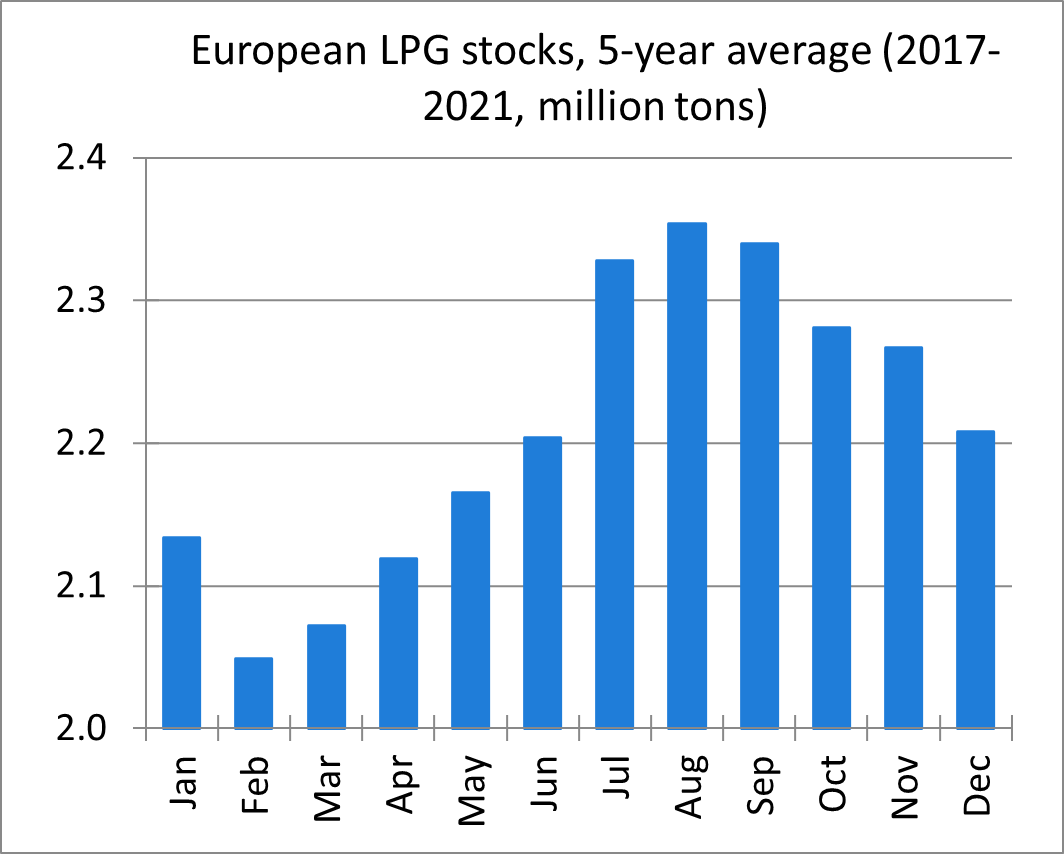

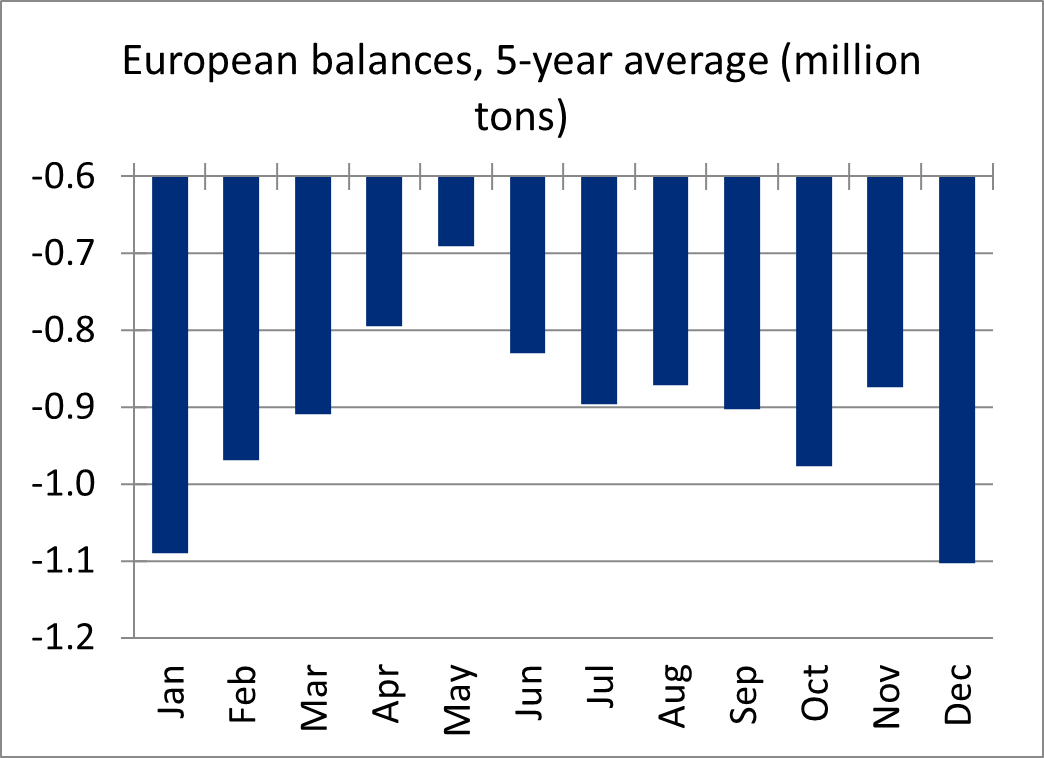

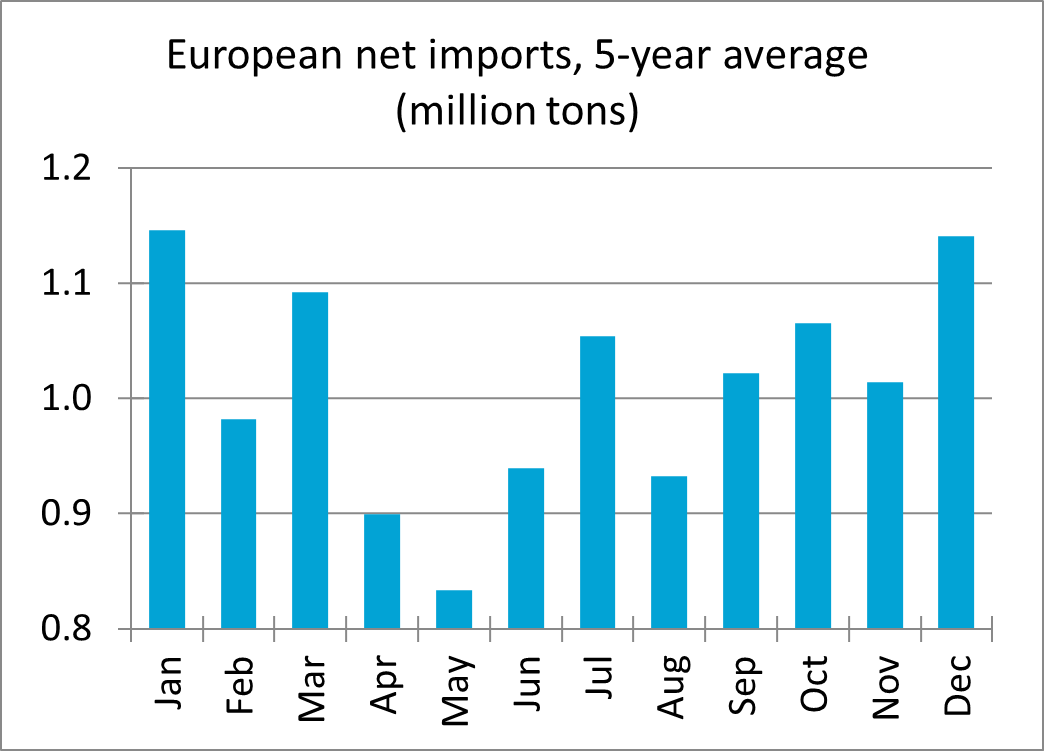

In any case, on average, that leaves just the months April to August each year relatively risk free from supply or shipping disruptions relating to U.S. LPG exports. European balances are typically at their widest during the peak heating months of December and January when net imports are also seasonally at their peak, according to JODI data’s five-year average.

Source: JODI, OPIS

Source: JODI, OPIS

Outlook by Ciaran Tyler, Senior Analyst, ctyler@opisnet.com

OPIS developed the pricing in its Europe LPG & Naphtha Report to reflect the market’s desire for an unbiased methodology and accurate spot price benchmark in northwest Europe and the Mediterranean. Try the OPIS Europe LPG & Naphtha Report free for 21 days. You’ll get a daily PDF report plus alerts sent to your inbox as news breaks.