Retail Gasoline & Diesel Prices See Difficult Spring Profit Margins

Gas station operators, distributors and retailers were likely glad to see spring 2018 fade into the past.

The season lived up to its typically uneven nature, but OPIS data suggested that for most fuel marketers it was a more challenging 93 days than what has become standard in recent years.

Here’s an overview:

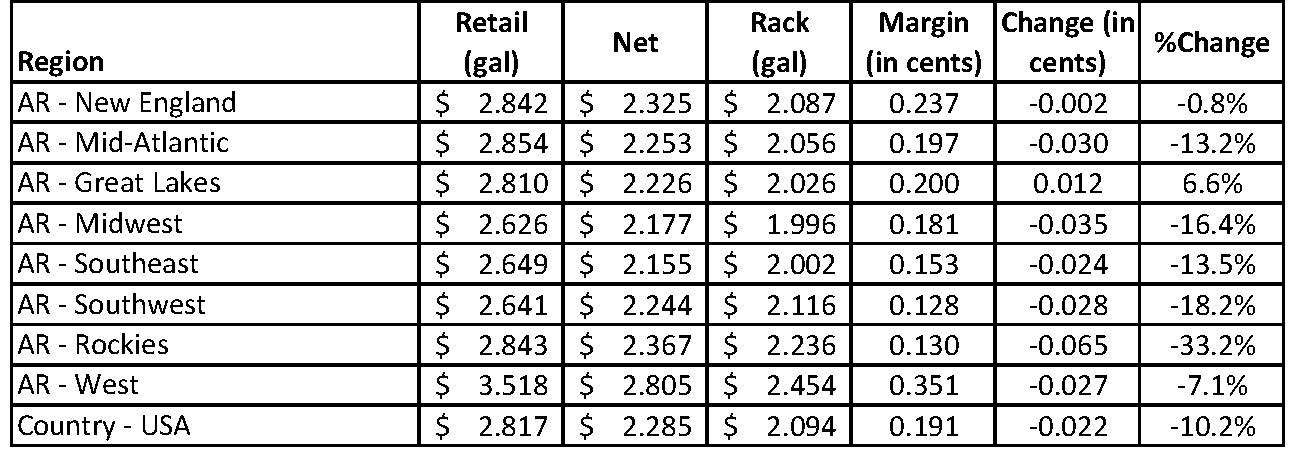

- On a nationwide basis, gasoline margins were off 10.2% with a particularly rocky performance in Rocky Mountain states, thanks to some refinery issues in Utah and Montana.

- States that historically saw gross margins of 20-25cts/gal instead saw that gap slim down to just 13cts/gal, thanks to stronger wholesale prices that couldn’t readily translate into higher retail gasoline prices.

- Only one portion of the country, the Great Lakes region, saw higher spring margins than a year ago.

Spring 2018 Retail Gasoline Price Margins At-A-Glance

Read more about retail markets and margins.

High Gasoline Prices Contributed, But Demand Played a Role

Higher prices, particularly in comparison to 2016 and 2017, were only part of the problem.

The Energy Information Administration implied consumption close to previous year levels, but OPIS’ survey of some 15,000 stations presented a different picture.

Every area saw declines, the OPIS Demand Report showed. Weather may have contributed to that trend.

Check out these factoids:

- The national measurement implied a slip of 2.4% from spring 2017.

- PADD5 (including Rocky Mountain states) showed the largest decline of 3.3% in volumes.

- Northeastern demand measurements dropped by 1.8%

- The Southeast fell 2.35%

- The Midcontinent eased 2.8%

- Southwestern demand slumped by 2.7%.

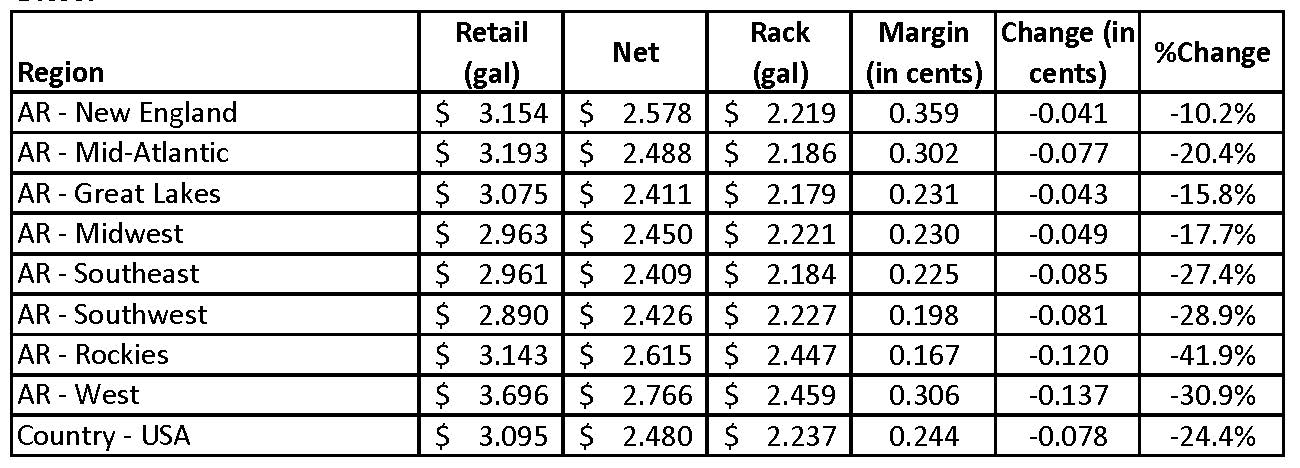

Don’t Forget About Retail Diesel Prices

Nationwide diesel margins were also victims of soaring wholesale prices and a very competitive retail market.

The average rack-to-retail gross margin for diesel fell a whopping 24.4% and every single region of the country participated in the downturn. Once again, the Rocky Mountain states topped what amounts to a misery index, with margins falling by 12cts/gal or 41.9% from 2017.

Some other highlights of an OPIS deep dive into spring retail fuel data:

- Shell maintained a hefty lead in branded site counts with just over 13,800 stations flying the Shell pecten. Its unleaded regular was priced about 3.4cts/gal above competitors.

- Chevron retailers pursued a practice of pricing well above other marketers, thanks in large part to its western footprint. A Chevron station typically priced unleaded regular at 8.29cts/gal above average numbers.

- Spring 2018 began on a very weak note with nationwide gross margins of just 11.7cts/gal and that stood as the lowest point in the period. The best of times occurred from June 16-18, when margins topped 30cts/gal for a brief period.

Postscript: The beginning of summer 2018 brought mixed news. Good news for marketers arrived in the form of an average 26.2cts/gal gross margin. The bad news was that that period still trailed the same days last year by 8.4%.

Determine how well your retail gas station volumes perform using the OPIS Demand Report, the only weekly resource for detailed retail fuel station volume data.