Voluntary Carbon Markets Stakeholders Play Hot Potato With Market Risk

With the integrity of carbon offsetting under fire, buyers are looking to lock down the forward delivery of high-quality credits from trusted climate projects, but there’s just one problem: some offset project developers don’t want to play ball.

From accusations that climate projects have disadvantaged local communities to claims of fraudulent carbon credit issuances, market proponents have weathered a hail of criticism in recent months. In response, some corporate buyers have ramped up purchasing due diligence and pushed for contracts that guarantee a fixed volume delivery over time.

This last point has given some sellers pause, such as Kennemer Eco Solutions Co-Founder and Technical Climate Lead Florian Reimer.

“For us, as a new market entry developer with only two projects, we would never sign such a liability,” Reimer said. “I think many smaller developers would feel uncomfortable with that.”

Hunting High-Quality Credits

During the last eighteen months, the voluntary carbon market has been characterized by trade illiquidity and a slump in prices after growth surged through the first half of 2022.

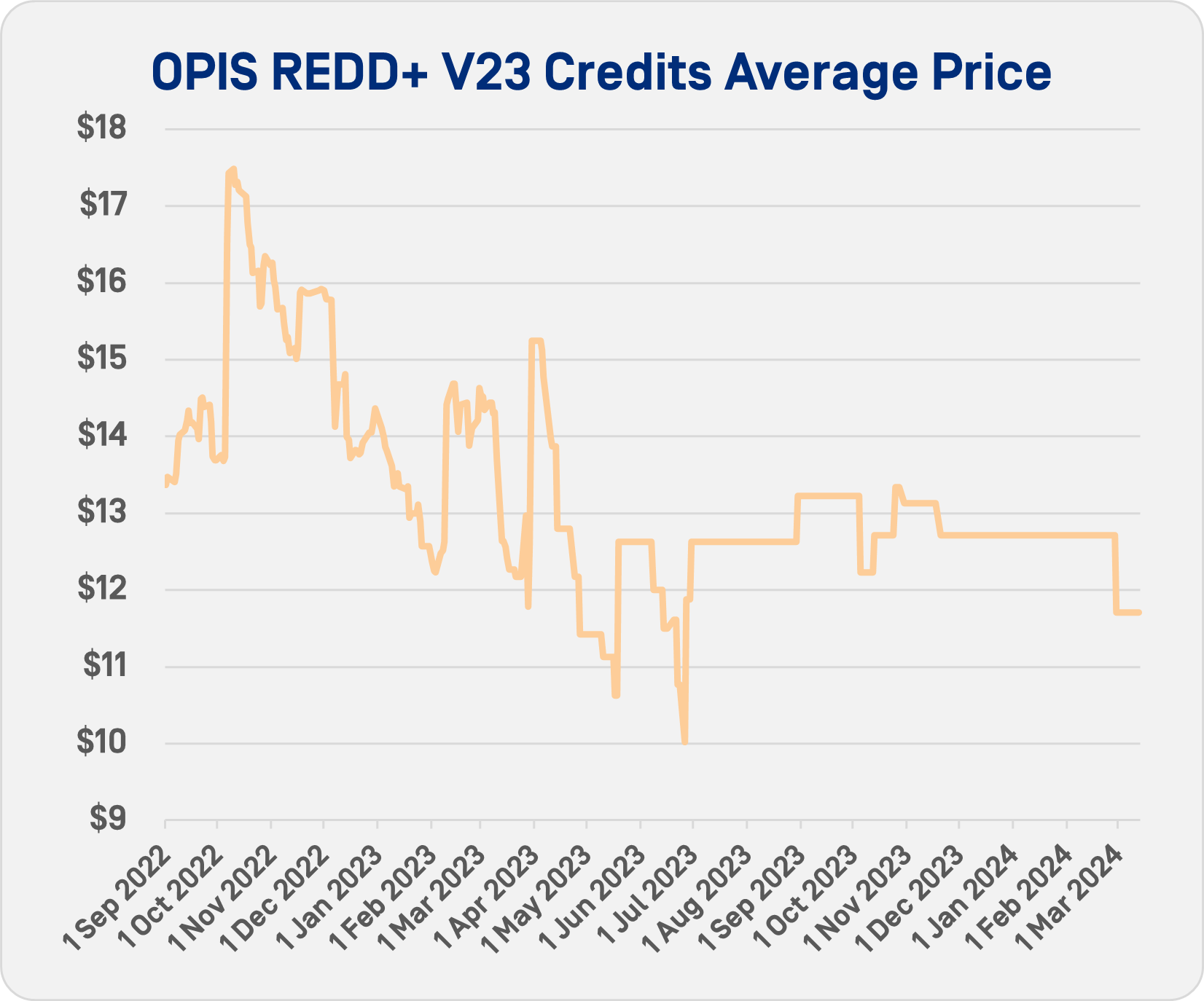

The OPIS Voluntary REDD+ Credits Average current-year price declined to below $12.50/mt in March 2024 from a peak of above $16/mt in October 2022.

The OPIS Voluntary REDD+ Credits Average current-year price declined to below $12.50/mt in March 2024 from a peak of above $16/mt in October 2022.

According to analysts, corporate purchasers are growing more careful.

Project developers have mostly kept up with bolstered demand for high-quality credits, but that may be changing. Credit retirements across the five largest registries outstripped issuances in 2024 until the last week of February. As of March 10, 48.2 million credits had been issued and 42.2 million had been retired.

Current market dynamics also reflect scientific debate over emissions reduction baselines and the volume of carbon that projects sequester, as exemplified by reporting in January from U.K. news outlet The Guardian.

Conditions have been exacerbated by the fact that the voluntary carbon markets are still structurally and operationally underdeveloped, sources said.

The Rocky Road to Project Revenue

It can take several years of work and significant investments before a climate project yields any income.

Climate projects are often built in a shifting, dynamic landscape, prone to upheaval from natural and human forces, and verifiers can only estimate potential emissions reductions. Actual credit issuances might significantly exceed or miss those expectations.

If a project is sufficiently capitalized, this last point is irrelevant because the developer can afford to wait for credits to be issued before it sells them.

But if a developer needs to fund operations before credits are issued, it may sign contracts that promise credit delivery on a forward basis.

The Role of Forward Delivery

Industry stakeholders generally agree that forward delivery contracts can play a crucial role in developing the market. But once the details of forward emissions reduction purchase agreements come into focus, buyers and sellers sometimes find themselves at odds.

One key sticking point involves the volumes of credits delivered. Some ERPAs (known as proportional forward ERPAs) require the project developer to deliver a percentage of the credits they ultimately issue. Others prescribe a fixed volume for future delivery (and are known as fixed forward ERPAs).

For a fixed forward contract, a developer must make up the difference if their project doesn’t produce enough credits to fulfill the order.

“New carbon projects launched by smaller developers are high-risk ventures,” Reimer said. “The buyer or investor is usually the financially stronger party.

“This is an early-stage capital investment associated with high returns but also high risks,” Reimer added. “I think smaller developers argue that those parties need to carry the risk of delayed issuances, and traditionally that has been the majority of cases. We find no problem in financing our projects via forward contracts without a replacement credit liability.”

Fixed forward contracts, however, are becoming more commonplace, and developers’ ability to avoid such circumstances may be shifting.

In February 2023, the International Emissions Trading Association released framework ERPAs intended to serve as a blueprint. The IETA forward ERPA included language that secures fixed forward delivery.

If a carbon offset credit shortfall “beyond the reasonable control of the Seller” occurs “the Seller shall instead be obligated to Transfer Comparable VCCs in an equal number to the shortfall and otherwise in accordance with this Agreement as soon as reasonably possible,” according to the document.

This Primary ERPA (along with a related Contingent Secondary ERPA) “is intended to provide a minimum benchmark for transacting emissions reduction and removal credits by including basic provisions relating to the transaction of such credits,” according to an IETA news release.

Are Strong Risk Protections Counterproductive?

The company Respira manages a portfolio of high-quality voluntary carbon offset credits. According to CEO Ana Haurie and Director of Business Development Will Close-Brooks, it prefers to sign proportional, not fixed, forward ERPAs.

“When you’re trying to contract on a forward basis, you need to build risk mitigation into your arrangements,” Haurie said. “We just need more certainty. I hope that high-quality project developers won’t be put off one way or the other.”

Close-Brooks said, “We want the project [with which we transact] to continue to be viable and to be successful. So, I would say we’re very interested in mutually sharing risk and trying to be pragmatic.”

Mike Korchinsky, whose conservation organization Wildlife Works is primarily funded through REDD+ credit sales, sees another wrinkle in this dialogue.

“We believe in market mechanisms,” Korchinsky said. “We have seen the evolution of the market from its origin. [Fixed forward ERPAs] are going to work well for high-volume buyers in the global North. Oftentimes, that’s at odds with the people who actually bear the cost, the true cost of change.”

In Korchinsky’s view, the local and indigenous communities that often must change their way of life to support a project are too-often ignored in transactions. If too many deals occur that don’t adequately serve their needs, they could grow reluctant to collaborate.

“Imagine a community that has begun work on a carbon project,” Korchinsky said. “It hasn’t received any funding for the work it has done. Then the project doesn’t deliver for whatever reason. They can be held accountable to the buyer for the market value of replacement credits. It’s not malicious; it’s short-sighted. If the buy side tries to be too self-serving, it can be counterproductive.”

Voluntary carbon credits forward delivery contracts are unique for another reason. Unlike other sectors, the contracts can’t be easily used to secure funding from a third party. That reality has frustrated ALLCOT CEO and Founder Alexis Leroy, whose business develops both renewable power and carbon offset projects.

“If I were building renewable power, I could get a power purchase agreement, walk into the bank the next day, and they would finance 75%, 80% or maybe even more than 100% of the project,” Leroy said. “But with an ERPA, no bank in the world would provide us with capital.”

Risk Tools, Insurance Enter the Picture

Still, the IETA ERPAs only represent a starting point in negotiations. Contracts signed by sellers and buyers tend to be highly specific depending on project specifications. Forward carbon offset insurer Kita CEO Natalia Dorfman has witnessed this firsthand.

“Any time you negotiate a contract where the two parties don’t necessarily have a view of what everyone else in the market is doing, you create the potential for imbalances on either side,” Dorfman said. “I’ve seen ERPAs that are wholly unfair to the project developer. I’ve seen somewhere the buyers are taking on significant amounts of risk. And I’ve seen others that are less than a page in total. One of the key challenges within the market is that it lacks the basic underpinnings it needs to scale.”

Contract reform, furthermore, isn’t the only tool stakeholders have at their disposal. Insurance providers, including Kita, Parhelion, Howden Group Holdings, Oka and others, have begun to underwrite aspects of VCM projects and transactions.

“Even with the best ERPA, all it can do is pass risk up or down the chain, ultimately to the buyer or the seller of the offset,” said Parhelion CEO Julian Richardson. “The problem with this is that contract counterparties might not be willing or able to accept the risk. There is no point forcing your counterparty to accept the risk if their balance sheet is limited or they are not creditworthy. By bringing highly rated insurance paper to the table, we are giving counterparties a creditworthy third party to transfer the risk to.”

A number of carbon credit ratings agencies, such as Calyx Global, Sylvera and BeZero have also launched to provide third party credit quality information.

“In terms of securing future ‘quality’ supply, this is a super interesting topic,” said BeZero CEO and Co-Founder Tommy Ricketts. “The surge in pre-issuance market activity, notably for engineered and nature-based removals, has come with rising calls from our clients for pre-issuance risk tools. Not surprisingly that’s something we are investing in heavily. I think that will be a big trend for 2023.”